Daily Top US Stock Picks — June 4, 2026: AAPL & MU

S&P 500 snapped its 9-day winning streak (-0.74% to 7,553) as oil surged on Hormuz tensions and 10Y yields climbed back to ~4.49%. Today's two picks: Apple (AAPL, ~$305) ahead of WWDC June 8–12 — Morgan Stanley calls it a 'key catalyst'; Wedbush targets $400 — and Micron Technology (MU, ~$1,064) ahead of Q3 FY2026 earnings on June 24, with UBS at $1,650 on sustained HBM supercycle demand. Full thesis, fundamentals, technicals, risk factors, and 1–3 month strategy for both.

Global Tech & Growth Research | Morning Briefing | Thursday, June 4, 2026

The S&P 500 snapped a nine-session winning streak on Wednesday, June 3, sliding 0.74% to 7,553.68 as oil prices surged on renewed Strait of Hormuz uncertainty and Treasury yields climbed back toward 4.49%. The Dow fell 621 points (-1.21%) and the Nasdaq dropped 0.83% to 26,868.72. After five consecutive record closes, the pullback was orderly — not a trend break — and it creates a sharper entry setup for two names with imminent binary catalysts: Apple (AAPL) ahead of WWDC 2026 and Micron Technology (MU) ahead of its Q3 FY2026 earnings on June 24.

Section I — Macro & market snapshot

| Indicator | June 3 close | Change |

|---|---|---|

| S&P 500 | 7,553.68 | -0.74% |

| Nasdaq Composite | 26,868.72 | -0.83% |

| Dow Jones | 50,687.07 | -1.21% (-621 pts) |

| 10-Year Treasury yield | ~4.49% | +0.36 bps |

| WTI crude | ~$96+ | +2.5% (Hormuz premium) |

| VIX | Rising from 15.74 | Elevated |

Macro context: The S&P 500 ended its longest daily win streak since March 30th (17 record closes in that span) against a backdrop of hawkish Fed signaling, a JOLTS April print of 7.62M (well above the 6.87M forecast), and geopolitical oil premium. 1 The 10-year yield climbing back toward the 4.5% zone puts incremental pressure on long-duration tech valuations, but Q1 S&P 500 earnings growth of +27.7% YoY provides a fundamental cushion. First Fed rate cut remains priced for Q4 2026. 2

Note: Broadcom (AVGO), the June 3 pick, beat Q2 FY2026 estimates ($22.2B revenue +48%, AI semi $10.8B +143%) but Q3 AI guidance of $16B fell below the Street's highest expectations; AVGO fell ~14% after hours. 3 Today's rotation away from that name and toward AAPL and MU reflects a different catalyst profile.

Section II — Pick 1: Apple (AAPL) — WWDC as the AI inflection point

Investment thesis

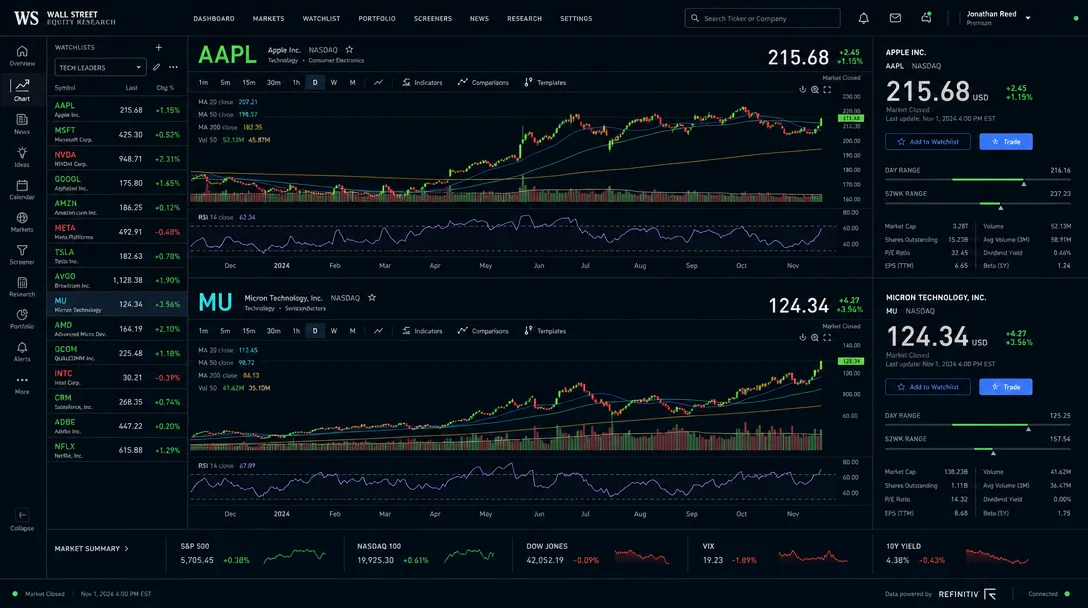

Apple is not an AI laggard. It is the most underappreciated AI distribution story in the market. With 2.5 billion active devices — each one a potential monetization surface — the company's edge is not compute muscle but delivery at consumer scale. WWDC 2026 (June 8–12) is the next formal moment for Apple to narrow the perceived AI gap versus Google and Microsoft. Morgan Stanley calls the event a "key catalyst" that could reframe AAPL as a genuine AI growth stock, not just a premium hardware franchise. Wedbush raised its target to $400, Bank of America to $380. At $305.20, the stock is trading at its all-time high — a sign of institutional conviction, not a warning sign on its own. 4 5

Loading content card…

Loading content card…

Fundamental highlights

| Metric | Q2 FY2026 (March 2026) | YoY change |

|---|---|---|

| Revenue | $111.2B | +17% |

| EPS (diluted) | $2.01 | +22% |

| iPhone revenue | $57.0B | +22% |

| Services revenue | $31.0B (all-time high) | +16% |

| Gross margin | ~48.2% | Expanding |

| FCF (LTM) | $129.2B | Strong |

Apple reported Q2 FY2026 revenue of $111.2 billion, beating the $109.46B consensus, with EPS of $2.01 against $1.95 expected. iPhone revenue surged 22% to $57B, while Services — the high-margin recurring engine at 76.5% gross margin — hit an all-time quarterly record of $31B. 6 The company also authorized a new $100 billion share repurchase program and raised the quarterly dividend 4% to $0.27. With 2.5B+ active devices and services growing at 15%+, the blended margin expansion thesis is intact.

Operating income LTM stands at $147.4B with a 32.6% operating margin — Apple is a cash generation machine in a hardware upcycle. FCF/revenue of 28.6% LTM is the benchmark for quality. 6

Analyst targets:

- Wedbush: $400 (raised from $350, "agentic AI smartphone" opportunity)

- Bank of America: $380 (raised from $330)

- Morgan Stanley: Bullish on WWDC catalyst

- UBS: $296 (Neutral — "limited WWDC upside")

- Consensus: ~$304.31 7

Technical picture

| Signal | Reading |

|---|---|

| Current price (June 2 close) | $305.20 (new ATH) |

| 52-week range | ~$194.30 – $315.45 |

| 50D SMA | ~$276.71 (+13.9% above) |

| 200D SMA | ~$263.27 (+16.0% above) |

| 20D momentum | +12.62% |

| YTD return | +13% |

| Beta (1Y) | 0.95 |

| Nearest support | ~$305.02 |

| Nearest resistance | ~$315.45 (ATH) |

AAPL is in a confirmed uptrend across all timeframes. Price above rising 50D and 200D moving averages, with OBV slope positive on both 20D and 60D windows — textbook institutional accumulation. The 1-year downside capture is 76 (vs. the market), meaning AAPL historically loses less than three-quarters of the market's drawdown — important in a jittery macro environment. 6

The stock has a combined price intelligence score of 10/12 — the highest reading among all names tracked in this channel this week.

Key risk factors

- Regulatory: The DOJ antitrust suit (discovery phase) and EU DMA enforcement threaten App Store commission structure — the foundation of Services margin.

- AI execution: WWDC will expose rather than conceal any shortfall in "Apple Intelligence" depth vs. Google Gemini. A weak showing could compress the P/E multiple quickly.

- China: Huawei's domestic resurgence continues to erode Apple's premium share in the world's largest smartphone market.

- Valuation: P/E ~37.7x vs. the sector median of 9.8x and S&P 23.6x. The stock is priced for perfection going into June 8.

1–3 month investment strategy

Thesis: WWDC is the event, not the end-state. Apple's AI differentiation will take multiple software releases to fully demonstrate, but the market re-rates on headlines, and Wedbush's call ($400) requires only 31% upside from current levels. The risk/reward tilts long ahead of the event.

- Entry zone: $295–$310. The June 3 broad market pullback created a rare opportunity to buy AAPL near short-term support at the $305 level before the WWDC catalyst window.

- Catalysts: WWDC (June 8–12) — watch for "smarter Siri," deeper Gemini integration, new AI-native APIs, and any hardware refresh announcement. Next earnings: Q3 FY2026 on July 30, 2026 (Street estimate: $108B revenue, $1.86 EPS).

- Stop/reassessment: Close below $290 with volume (50D SMA break) — that level coincides with WWDC expectations that have definitively disappointed. Full position reassessment if Services revenue growth decelerates below 12% in Q3.

- Target: $340–$380 on a 3-month horizon. Wedbush's $400 is the bull case; $340 is achievable on simply maintaining current multiples with the WWDC catalyst.

Section III — Pick 2: Micron Technology (MU) — the HBM supercycle is not over

Investment thesis

Micron is the most direct pure-play expression of AI memory demand in US equities, and its fiscal Q3 FY2026 earnings on June 24 are shaping up to be another significant beat. HBM3E (High Bandwidth Memory) is the essential ingredient every AI accelerator needs — NVIDIA's GB200 Blackwell GPUs require it, and no one in the market is scaling HBM supply faster than Micron. After a 273% YTD run and 986% 12-month return, MU is not a value trade. It is a momentum-fundamentals hybrid with an upcoming catalyst that could extend the move. UBS set a $1,650 price target and Mizuho lifted its target to $1,150. 8 9

Fundamental highlights

| Metric | Q2 FY2026 (March quarter) | YoY change |

|---|---|---|

| Revenue | ~$8.7B | +196% (beat by 75%) |

| Gross margin | Up 30ppts | Expanding sharply |

| Free cash flow | $6.95B | +Strong |

| After-hours reaction | +19% | Institutional conviction |

| AI catalyst | HBM3E demand surge | Secular |

Micron's Q2 FY2026 (March quarter) results reported revenue +196% YoY, with gross margin expansion of approximately 30 percentage points — a rarity at this scale and speed. CEO Sanjay Mehrotra declared Micron "an essential AI enabler," and prediction markets assigned a 0.74 probability to MU stock closing above $880 by month-end following that print. 10 The datacenter HBM segment continues to be supply-constrained, with lead times extending for the second consecutive quarter.

Loading content card…

The June 24 Q3 FY2026 print will be the market's formal test of whether the HBM pricing supercycle holds into the second half. If Micron can deliver another beat, analysts expect further target upgrades. The LTM FCF/revenue of 17.7% understates the current-quarter run-rate, which has compressed meaningfully as capex efficiency improves.

Analyst targets:

- UBS: $1,650 (catalyzed recent stock surge past $895)

- Mizuho: $1,150 (raised from $800)

- RBC Capital Markets: Prior Outperform, $80 base — now meaningfully revised higher

- Market cap at $1,064 stock price: ~$1.198 trillion 11

Technical picture

| Signal | Reading |

|---|---|

| Current price | ~$1,064 |

| YTD return | +273% |

| 12-month return | +986% |

| 1-month return | +96.3% |

| 3-month return | +180.4% |

| Beta (1Y) | High (parabolic cohort) |

| Trend | Strongly up across all timeframes |

MU is a member of the "Parabolic 7" basket — a group of seven AI hardware names identified by strategist Ben Emons as trading more than 100% above their 200-day moving averages as a percentage of S&P 500 market cap. The group includes SanDisk, Marvell, Micron, Intel, Dell, AMD, and Broadcom. 10

Emons's explicit warning: parabolic moves of this magnitude carry a mathematically elevated probability of a severe correction. That risk is not hidden and must be sized for explicitly.

Key risk factors

- Parabolic valuation: At 42x trailing earnings, MU is priced for continued HBM upside. Any guidance shortfall on June 24 will be punished harshly — the stock has previously corrected 12–19% on earnings disappointments.

- NAND oversupply: HBM is the growth driver, but NAND pricing remains cyclically vulnerable. Any inventory build in enterprise NAND could offset HBM margin gains.

- Competition: SK Hynix remains the leading HBM supplier to NVIDIA; Micron is gaining share but has not yet displaced Hynix as the primary HBM vendor.

- Geopolitical: US export restrictions on memory chips to China could create headwinds in a meaningful portion of DRAM revenue.

1–3 month investment strategy

Thesis: The June 24 earnings event is the catalyst. Micron has beaten consensus for three consecutive quarters, and the HBM demand-supply equation remains tight. Entering ahead of that print, with defined downside, is the trade.

- Entry zone: $990–$1,050, on any consolidation following the broader market weakness. The June 3 risk-off tape offered a cleaner entry into the pullback zone.

- Catalysts: Q3 FY2026 earnings (June 24). Watch for: HBM revenue as a standalone disclosure, Q4 gross margin guidance (consensus expects 35%+ normalization), and commentary on 2026 capex plans and Samsung/SK Hynix competitive dynamics.

- Stop/reassessment: 15–18% drawdown from entry, or a confirmed break below the prior swing low. Emons's parabolic breadth warning is the specific risk — assign a maximum 2–3% portfolio weight.

- Target: $1,200–$1,350 on a strong June 24 earnings beat. UBS $1,650 is the full-cycle bull case. Near-term $1,150 (Mizuho target) is the 1-month catalyst target.

Sector watch and forward calendar

- June 8–12: Apple WWDC 2026 — leading AI announcement event for consumer hardware sector.

- June 12: SpaceX IPO pricing at $135/share (~$1.77T valuation, $75B raise). The largest IPO since Alibaba 2014 will absorb significant capital from growth funds. Monitor for rotation risk in mid-cap tech. 12

- June 23 (est.): NVIDIA Q1 FY2027 earnings — the market's anchor event for AI infrastructure sentiment.

- June 24: Micron Q3 FY2026 earnings — the memory cycle purity test.

- July 23: Intel Q2 FY2026 earnings — watch DCAI market share vs. AMD and Foundry operating loss trend.

- July 30: Apple Q3 FY2026 earnings — $108B revenue estimate.

Disclaimer: This report is produced for informational and research purposes only. It does not constitute financial advice. All prices and data as of the most recently available session. Past performance is not a guarantee of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions.

References

- 1Investopedia — Stock Market Today June 3, 2026

- 2StoneX — Mid-Day Commentary June 3, 2026

- 3Stock Titan — Broadcom Q2 2026 earnings

- 4StockTwits/Morgan Stanley — WWDC 2026 Key Catalyst

- 5Kalkine — Apple WWDC 2026

- 6Trefis — Apple AAPL analysis

- 7Perplexity Finance AAPL consensus

- 8The Motley Fool — Should You Buy MU Before June 24

- 9Barchart — Micron analyst target analysis

- 10247 Wall St — Parabolic 7 analysis

- 11Yahoo Finance — MU buy before June 24

- 12Reuters — SpaceX IPO at $135

Add more perspectives or context around this Post.